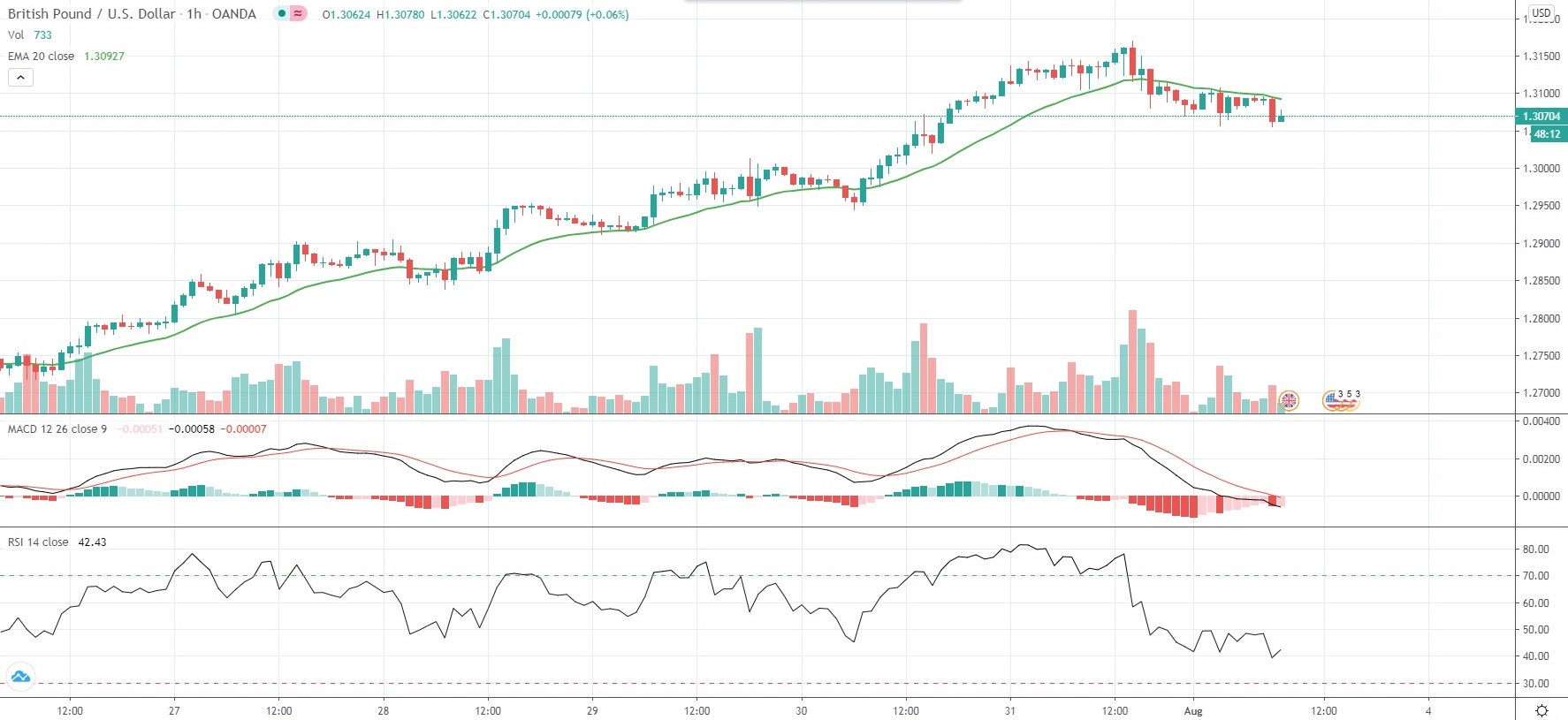

GBP/USD came off Friday’s 21-week highs and slipped back below the 1.3100 mark on Monday, as the US Dollar was attempting a rebound from more than two-year lows against peers ahead of fresh macro data.

The US Dollar has been under selling pressure due to concerns over slowing economic recovery amid rising COVID-19 infections across the United States, which also pushed US government bond yields to multi-year lows. The yield on US 10-year bonds dropped to 0.533% on July 31st, or the lowest level in at least 13 years, undermining the yield appeal of the US currency.

“…the dollar’s decline is likely to continue. Real U.S. interest rates are declining even as the country is running a big current account deficit, a situation we hadn’t have for a long time,” Minori Uchida, chief currency analyst at MUFG Bank, said.

Concerns over US outlook mounted after policy makers did not manage to reach an agreement on providing additional stimulus for the coronavirus-ravaged economy even as an expanded $75-billion-per-month unemployment benefit expired on July 31st.

White House Chief of Staff Mark Meadows said over the past weekend that he was skeptical about reaching a near-term agreement on the next round of economic relief from the pandemic.

Also on market players’ radar are escalating tensions between the United States and China on geopolitical, trading and technological fronts.

As of 7:04 GMT on Monday GBP/USD was inching down 0.09% to trade at 1.3073, while moving within a daily range of 1.3055-1.3107. On Friday it climbed as high as 1.3170, or a level not seen since March 9th (1.3201). The major pair advanced 5.52% in July, while marking a second straight month of gains and its best monthly performance since May 2009.

On today’s economic calendar, at 8:30 GMT IHS Markit/CIPS will release the final data on UK manufacturing activity for July. The respective Purchasing Managers’ Index probably came in at a final 53.6, according to market expectations, which would confirm the preliminary estimate. It indicated the strongest expansion in manufacturing activity since March 2019.

At the same time, activity in United States’ manufacturing industry probably expanded for a second consecutive month in July, with the respective Purchasing Managers’ Index coming in at a reading of 54.0, according to market expectations. In June, the gauge was reported at 52.6, indicating the sharpest rate of expansion since April 2019, as the sub-indexes of new orders, production and prices rebounded, while those of employment and new export orders dropped at a softer rate. The Institute for Supply Management is to release the official report at 14:00 GMT.

Bond Yield Spread

The spread between 2-year US and 2-year UK bond yields, which reflects the flow of funds in a short term, equaled 20.4 basis points (0.204%) as of 6:15 GMT on Monday, up from 18.3 basis points on July 31st.

Daily Pivot Levels (traditional method of calculation)

Central Pivot – 1.3109

R1 – 1.3147

R2 – 1.3209

R3 – 1.3247

R4 – 1.3286

S1 – 1.3047

S2 – 1.3009

S3 – 1.2947

S4 – 1.2886