Key moments

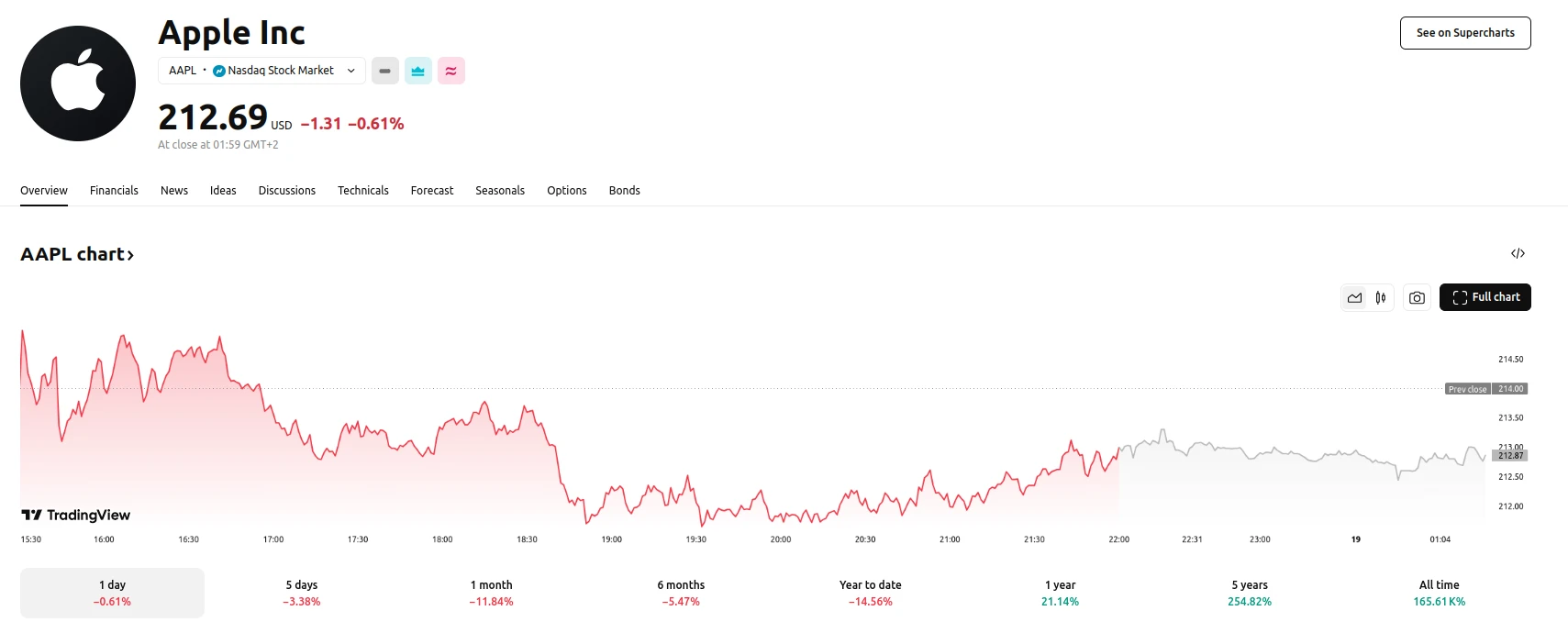

- Evercore ISI analysts raise Apple’s price target to $275, citing its position as a “tech staple” and potential AI beneficiary. As of March 19, 2025, Apple shares are down -0.61%, to 212.69 USD.

- Analysts predict sustainable mid-single-digit revenue growth and low-to-mid-teen percentage growth in EPS and free cash flow for Apple.

- Evercore highlights Apple’s in-house chip design as a key advantage for AI monetization and margin expansion.

Apple’s AI Potential and Financial Stability Drive Analyst Optimism

Evercore ISI analysts have reaffirmed their bullish stance on Apple, increasing their price target to $275, based on the company’s strong fundamentals and its potential to capitalize on the burgeoning artificial intelligence market. The analysts’ report, the fifth annual Apple Primer, emphasizes the company’s ability to maintain its position as a “tech staple,” with projections of consistent revenue growth and robust financial performance. This optimistic outlook is underpinned by Apple’s strategic focus on in-house chip design and its ability to monetize AI technologies without significant capital expenditure on specialized hardware.

The analysts anticipate that Apple will achieve sustainable revenue growth in the mid-single-digit percentages over the next several years. Furthermore, they project that earnings per share (EPS) and free cash flow will experience low-to-mid-teen percentage growth during the same period. Evercore believes that the market frequently underestimates Apple’s ability to drive growth through product mix, pricing strategies, operational efficiency, and share buybacks. Notably, the analysts highlight Apple’s proficiency in developing custom chips as a crucial factor in its AI strategy. By leveraging its expertise in chip design, Apple can enhance product functionality and improve gross margins, particularly in the context of AI applications.

The report also points to several growth catalysts for Apple, including the increasing demand for next-generation devices with integrated Apple Intelligence features. The analysts anticipate that consumer upgrades will drive iPhone and Mac sales, while the App Store’s revenue from AI-related subscriptions will provide an immediate benefit. Additionally, Apple’s expansion into emerging markets, such as India, and the growing popularity of its wearable devices, including the Apple Watch, present further opportunities for growth.

Evercore’s analysis suggests that Apple’s commitment to returning capital to shareholders, coupled with its consistent financial performance, will contribute to reduced stock volatility and sustained valuation.